TL;DR: Starting a short-term rental business can be highly profitable — the global market was valued at $134 billion in 2024 and is projected to nearly double by 2030. Success depends on choosing a high-demand location, understanding local regulations (which are tightening in many cities), deciding whether to self-manage or outsource, and securing the right insurance and damage protection. Key steps include registering your business, listing on the right platforms, pricing dynamically, and continuously optimising based on guest feedback.

When you enter the short-term rental business for the first time, there’s a lot to think about. You might not have a clear picture of what your future will look like just yet. All you know is you’ve got a dream and you’re ready to make it happen.

That’s where we come in. With a little insider knowledge, you’ll be set up to earn more, stress less, and protect your investment for the long term. In this article, you’ll learn about:

- Creating a short term rental business plan

- Short term rental tips for property managers

- Licensing and regulations

- Steps for setting up a short term rental business

- How to run a short term rental business and optimize for profits

Should you start a short-term rental business?

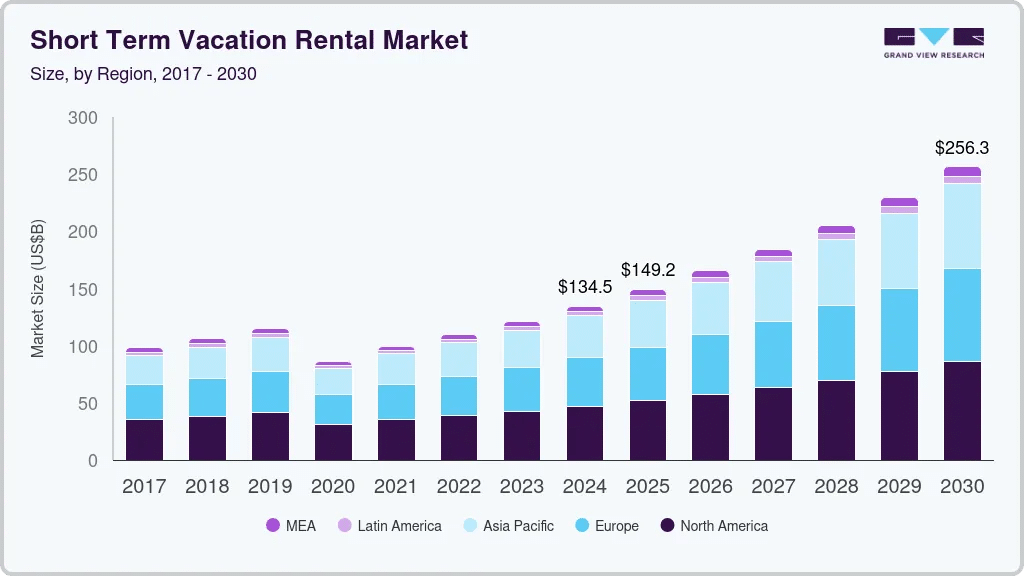

While many of us have felt the economic squeeze of recent years, the global short term vacation rental market has been growing. It was valued at 134.51 billion USD in 2024, and is projected to reach 256.31 billion by 2030.

Innovations like guest management and dynamic pricing have given hosts better tools to manage their businesses and ensure more stable income. Meanwhile, tourism has rebounded since the COVID-19 pandemic, particularly for “digital nomads” who have the ability to work remotely.

In short, it’s a good time to get into business. But it’s always worth considering whether it’s the right model for you as a property owner.

It’s generally easy to advertise your property on platforms like Airbnb, Vrbo, and Booking.com. You can absolutely manage your Airbnb remotely, but you still need to market your property and manage guest communications, which can be more work than you’d expect.

Why consider starting a short-term rental business?

Short-term rentals function similarly to hotels but can feel less impersonal for guests, and more hands-on for hosts. Running your business this way can feel high effort, high reward, depending on what you value. For example:

- You meet people from all over the world. You might enjoy interacting with different people and helping them discover your local area.

- You get a vacation home that pays for itself. If you’ve sussed out the best place to buy a second home in Europe you can visit when you want and rent it out for the rest of the year.

- It can be totally flexible. You can limit availability when your life or strategy changes, and adjust the pricing dynamically based on season, events, or demand.

- You get control over your property. Set house rules for guests to follow and use guest screening services to vet who stays in your property.

- Equity grows faster. Short-term rentals can be very profitable. If your income exceeds long-term rent, you can pay the mortgage on your property faster.

Is a short-term rental business profitable?

Compared to renting your property long term, short-term rentals do come with added upfront costs for furnishings and amenities, as well as regular cleaning costs. Just look how much Airbnb property managers charge to get an idea.

That said, a short-term rental business can be more profitable than long term renting.

Short term rentals boast a high nightly income on average, thanks to dynamic pricing tools that automatically adjust your rate to meet demand. They may even come with more tax advantages, depending on where you’re based, such as more deductible categories.

Of course, your profit will depend on your short term rental business model – so make sure you put time and effort into your business plan, or enlist help from a professional. You may also need to consider damage protection services through a provider like Truvi, to help protect your investment from unexpected guest damage.

Ready to start or expand? Check out the best places to buy a vacation home around the world.

Which short-term rental business model is right for you?

Before you start planning, it’s worth deciding how you actually want to enter the market. There are three main routes:

Buy your own property

The most capital-intensive option, but you own the asset and keep the returns. Requires solid research into local demand, STR regulations, and ROI before you commit.

Rental arbitrage

You lease a long-term rental and sublet it short-term at higher nightly rates. Lower upfront costs, but you’ll need your landlord’s permission and a clear-eyed view of the margin between your rent and your projected income.

Property management or co-hosting

You manage someone else’s property in exchange for a percentage of revenue. No property investment required — but you’ll need to demonstrate you can handle marketing, guest communications, and operations before owners hand you the keys.

Many hosts start with management or arbitrage, build up experience and capital, then move into ownership. There’s no single right answer — the best model depends on how much you’re able to invest, how hands-on you want to be, and how quickly you want to scale.

How to create a short -term rental business plan

Starting a short-term rental business isn’t as simple as putting up a listing online. It’s about managing a property like a full-scale business – because it is one. Start by mapping out your short term rental business plan, so you can identify any opportunities or blockers before it’s too late.

1. Choose a location and start market research

It’s essential to pick an area with enough demand to sustain your business. National and regional tourism boards often release statistics that will give you a solid idea of visitor numbers and popular times of year in a particular area.

Is the area you’re looking at popular year-round, or does demand fluctuate seasonally? You’ll need to adapt your short-term rental strategy accordingly.

Consider popular tourist destinations as well as more up-and-coming areas – how might demand change over time? Are there significant events planned in the area that might affect it? Following one of the basic rules of economics, the best destinations for starting a vacation rental business will have both high demand for holiday lets and a low supply.

Here are some of the best cities for short-term rental businesses:

- Orlando, Florida, USA

- Boston, Massachusetts, USA

- San Diego, California, USA

- Brighton, UK

- Crete, Greece

- Berlin, Germany

- Bali, Indonesia

- Bangkok, Thailand

Short-term rental restrictions are becoming tighter in major cities – like New York and Barcelona. It’s worth considering whether restrictions might be imposed in your chosen area in the near future, particularly if it’s a place that has issues with housing or over-tourism.

Once you’ve landed on a location, consider other short -term rental properties in your area – how are they pricing their stays? If you’re in an area with plenty of competition, try to understand what factors might give your holiday rental an edge. For example, city flats in warmer countries might get overlooked if they don’t have air conditioning.

Consider what upfront costs you can manage without putting your finances at risk. Even small touches here and there could mean more profits in the long run – so investing in that new coffee machine might be the way to go.

2. Consider self-managing vs. outsourcing

If you’d rather outsource the whole headache of running a short -term rental, you can hire a property manager to take over. You’ll start earning passive income while they take care of the rest. The fees will feel worth it if your property manager always keeps your place booked at the best rate.

However, almost 80% of hosts prefer to do it themselves, according to an industry report by Hospitable, citing higher profitability (55%) and better oversight of guest interactions and maintenance (64%) as main reasons to avoid outsourcing.

Doing it all yourself is a big time investment, but you’ll save on management fees, keep control over your business, and develop closer guest relationships. Like many hosts, you might prefer this approach, provided you’re confident you can handle all the marketing, admin, and finances.

First of all, consider which resource you have more to spare: time or money? And do you have the skills you need to manage your business successfully by yourself? If not, can you run a hybrid model, where you outsource some aspects but not all?

For example, if you’re a superstar with a mop and bucket, you might prefer to save on regular cleaning fees by turning your property over yourself. Meanwhile, you can turn to technology or even an assistant to help you manage guests communications or your business finances.

Setting up your business: important steps to follow

There are plenty of factors to consider before you get the ball rolling on your short-term rental business, from advertising to amenities. To keep track of it all, a short-term rental startup checklist is crucial:

1. Comply with local regulations

In the face of housing shortages and over-tourism issues affecting major cities, regulations on short -term rentals are tightening around the world. Take a look at our guide to global short term rental regulations if you want to learn more.

Some cities are more short-term rental friendly, while others (like New York City) impose stringent restrictions. Depending on where you are, your local regulations may affect:

- The number of days guests can stay for at one time

- Whether or not you need to be a resident at the property

- Short-term rental licenses you need to apply for

- Whether the property needs to be furnished

- How many days a year the property needs to be let

- The tax you pay

- Whether you need to apply for planning permissions

This is certainly not an exhaustive list. Make sure you know what’s considered a short -term rental in your area and brush up your local regulations, as they might be different from those used in a neighbouring country or city.

Some cities, including San Diego and Henderson, NV, have made it easier for property managers to stay on top of regulations, with dedicated resources available online for short-term rental compliance. Meanwhile, short-term rental properties in Denver, in the US, have strict rules, including that the property must be the property manager’s primary residence.

Looking at the UK market instead? You’ll need to understand the specific UK legal requirements for short-term rentals.

Consider what taxes you’ll need to pay, too. This often depends on where your rental property is located and how your rental is run. For example, in the UK – a furnished holiday let (FHL) is taxed differently to other short-term rentals. However, FHLs must follow strict regulations on occupancy and amenities.

Start vacation rental business research early, as you’ll want to give yourself plenty of time to factor regulations into your budget. Plus, applications and paperwork can take a long time to be returned to you. You don’t want to risk operating without the proper licenses or permissions when you’re welcoming in your first guests.

2. Furnish the property and invest in amenities

Short-term rentals usually cater for tourists and other travellers who prefer a homely stay to a hotel. At a minimum, you’ll need to provide all the basic amenities your guests need to get by (this is also a necessary requirement for an FHL in the UK). Think: beds, seating, and basic kitchen facilities like a refrigerator.

But Airbnb’s tagline, ‘Live like a local’, is a nod to the fact that short term lets often provide much more than the basics. Tea and coffee, a spa bath, or even a bottle of wine and some cheese in the fridge might be part of the package in an Airbnb, depending on its price point.

Take a look at our list of 30 must-have amenities for an Airbnb for some inspiration.

3. Select the right platform to list your rental

Listing your property on a trusted, well-developed, and popular platform not only helps you reach potential guests – it can also provide you with the support you need for running your business. Here’s a closer look at some of the leading options:

- Airbnb: Synonymous with holiday renting, Airbnb offers a large user base, a range of dynamic pricing tools, insurance, and user-friendly features for both hosts and guests.

- Vrbo: Originally catering to vacation rentals, Vrbo is excellent for larger properties and family-oriented listings.

- Booking.com: Popular internationally, Booking.com is a good option if you want to attract guests from all over the world.

So, which is best? Arguably, Airbnb provides the most comprehensive features for hosts, from insurance to an efficient online booking process and dispute management. Its continued popularity means your property is likely to be seen by many potential guests, and the trust it has earned with people around the world rubs off on your business, too.

Don’t feel you need to stick to one platform, either. It may be worth listing a property on multiple to maximize exposure and occupancy.

4. Get STR insurance

Guests introduce variables that may not be covered under regular homeowners’ policies, such as accidental damage or theft.

Unlike traditional homeowners’ insurance, short-term rental insurance is designed to cover the unique risks associated with renting out your property. You’ll get some level of insurance included in bookings on Airbnb, Vrbo, and Booking.com, however, there are drawbacks. For example, Airbnb’s damage policy covers accidental damage and liability insurance, which is unusual, but you won’t be protected if you take bookings through your own website.

So, you may need additional insurance for direct bookings, as well as additional damage protections for bookings on platforms like Vrbo which only offer liability insurance. For example, Truvi can offer damage protection, which is included with our guest screening services and applies to all bookings regardless of which channel they come through. With the right policy, you can protect your property, minimize risks, and ensure peace of mind.

5. Optimize your rental for success

Once your property is live, the real work begins: making it stand out, optimizing occupancy, and ensuring a steady stream of positive reviews. Here’s how to how to run a vacation rental and make an impression:

- Staging and photography: High-quality photos and thoughtful property staging can make all the difference. Use professional photos to capture the best features of your space and ensure that your listing is visually appealing. Airbnb offers photography services to hosts, too.

- Set competitive prices: Price intelligently, and adjust for demand, seasonality, and competitors. Tools like Airbnb’s Smart Pricing or third-party pricing tools can help automate this process.

- Keep amenities updated: Consider keeping your amenities up-to-date as a part of your property’s maintenance. New, modern, functional features can add a special touch and keep your property aligned with changing guest needs.

6. Analyze and adapt your business strategy

Once your short-term rental is up and running, continuously monitor its performance. If you want to know how to run your vacation rental like a business – think in business terms:

- Track occupancy rates and revenue: Keeping an eye on occupancy rates and income generated per booking period will help you to understand peak times, allowing you to optimize pricing accordingly.

- Adapt to guest feedback: Take guest reviews seriously and implement improvements based on feedback. You’ll not only improve guest satisfaction but also boost ratings and visibility.

Return on investment (ROI), competition, and even branding are all worth thinking about if you want to set your listing apart. Platforms like Airbnb provide metrics on occupancy, revenue, and guest reviews, and these insights are essential for fine-tuning your strategy.

Ready to start your short term rental business?

There’s a lot to consider before you start your business, especially when missing an important step (like checking local regulations or getting damage protection) could have significant consequences in the long run.

But the short term rental industry is a dynamic one, which can be both exciting and rewarding for property managers.

If you love meeting new people from around the world, fancy yourself an interior decorator, or just want to make some extra income from your holiday home – a short-term rental business can be the dream job.

Protect your profits with Truvi

Carefully screen your guests and protect business from unexpected cleaning fees and accidental guest damage